Following one of the longest periods on record of small cap equities underperforming large cap equities, we believe small cap stocks have begun a long term recovery. In fact, small cap stocks have outperformed large cap stocks significantly since Liberation Day last year. The Russell 2000 Index is up 24.1% since April 1, 2025, over the 12‑month period, versus the S&P 500, which is up 16.3%. Although there has been concern about private credit, the public credit market has remained very strong this year, with only modest spread widening during the onset of the Iran war. High yield credit spreads are lower today than they were before the war began. Falling credit spreads have historically been positive for small cap equities, as strong credit markets enable access to capital for smaller cap companies and allow them to refinance future maturities at attractive borrowing cost.

Lower interest rates have supported the recent outperformance of small cap stocks. Interest rate cuts lower the cost of capital and interest expense which can accelerate earnings. Despite the recent performance of small cap stocks, they continue to trade at a large valuation discount to large cap stocks, whereas historically they have traded at a premium. Other factors favoring small caps include deregulation, increased mergers and acquisition activity, and benefits from a domestically focused budget bill. We expect small cap earnings growth to exceed large‑cap earnings growth for the first time in four years. Investment in small cap equities relative to large cap equities remains near historic lows. With the likelihood of sustained lower rates, a supportive credit market, attractive relative valuations, and potential for negative small cap sentiment to inflect positively, we believe now is the time investors will once again buy small cap stocks.

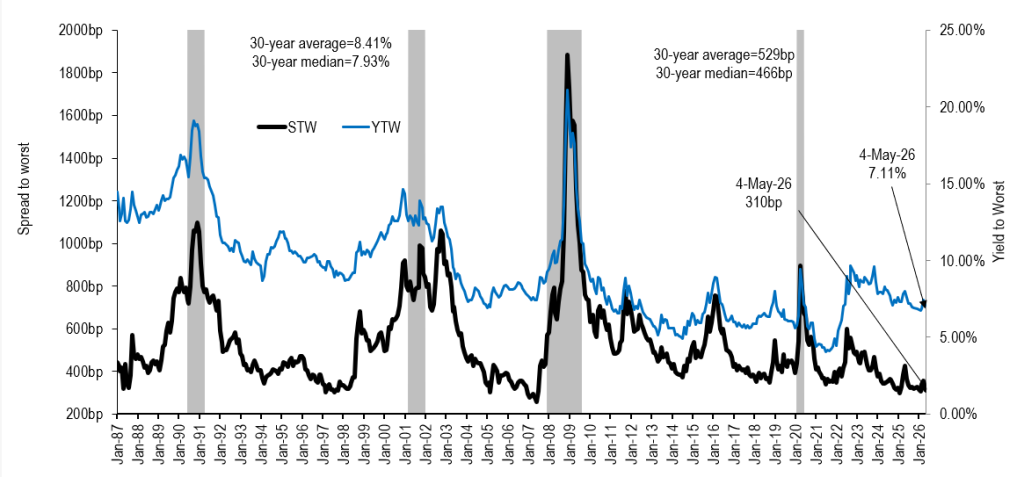

At Penn Capital, we have always focused on the entire capital structure of companies. We believe it is extremely important to fully understand each component of the capital structure when making investment decisions. How a company finances its balance sheet can determine both its success and the potential upside or downside in its stock. Historically, the credit market has been a leading indicator for small cap returns. We monitor the overall credit market to assess economic strength and equity market opportunity. As bond prices rise, the cost of capital for companies declines on the margin, which, all else equal, has the potential to increase present value. Equities, particularly small cap equities, tend to perform best during periods of stable or declining credit spreads.

Over the past two years, credit spreads, as measured by the Bank of America High Yield Index, have declined from over 500 basis points above Treasuries to below 300 basis points. The average spread in the high‑yield market since its inception has ranged between 400–500 basis points over Treasuries. Given that spreads today are below this range, the credit market is signaling a benign economic outlook. Typically, spreads reach at least 800 basis points over Treasuries when a recession is imminent. We do not believe spreads will reach that level due to the low default rate and strong financial characteristics of today’s high‑yield market. The high yield market remains in comparatively strong financial position relative to historical periods, with near record low default rates, a record high percentage of BB rated issuers, strong interest coverage ratios, and near record low leverage.

We believe the credit market is signaling a more favorable environment for small cap equities and the broader economy. Recessions are typically associated with credit crises, and we do not foresee a default cycle for several years. In our view, absolute valuations of small cap stocks are historically attractive, with some sectors still pricing in a recession. The relative valuation of small caps versus large caps remains near historic lows, and sentiment indicators for small caps are still very negative, meaning the recent improvement in small caps is still not largely appreciated by the market. Considering all these factors, we remain constructive on the outlook for small cap stocks.

Credit Spreads Indicate a Favorable Environment for Public High Yield

Source: JP Morgan as of May 2026.

The views expressed are those of Penn Capital Management Company, LLC, a boutique manager majority owned by Seaport Global Asset Management as of July 14, 2024. and are not intended as investment advice or recommendation. For informational purposes only. Investments are subject to market risk, including the loss of principal. Small cap securities may involve more risk than larger cap securities. Past performance does not guarantee future results. There can be no assurances that any of the trends described will continue or will not reverse. Past events and trends do not imply, predict or guarantee, and are not necessarily indicative of future events or results. Investors cannot invest directly in an index.