Joe Maguire, CFA

Sr. Portfolio Manager

Equity has a credit blind spot. 95% of Russell 3000 companies issue debt, 75% of which is sub-investment grade. Equity investors study stock price movements but often ignore credit market signals. However, when a company’s credit deteriorates, its equity follows.

Traditional equity research has a blind spot: Credit. 95% of companies within the Russell 3000 index issue debt, 75% of which is sub-investment grade*. Equity investors study the price movements on stocks but often ignore credit market signals. This is a mistake. If the credit of a company deteriorates, the equity will follow.

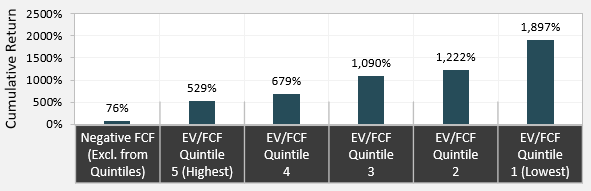

P/E, P/S, and P/B ratios ignore both outstanding debt and the cashflow statement, key components to a credit analysis. A better metric would be the EV/FCF ratio, which measures free cash flow generated to service debt and return cash to shareholders.

Companies with low EV/FCF multiples have historically exhibited outsized returns. While not a perfect metric, an EV/FCF analysis highlights the benefit of credit-equity research integration. Furthermore, low EV/FCF companies are positioned to benefit from the recent value shift that has been building momentum since October.

Russell 3000 Index: 20 Year Returns by EV/FCF Quintile

As of 10/31/2019. Source: Bloomberg. Enterprise value to trailing 12-month free cash flow, rebalanced monthly.

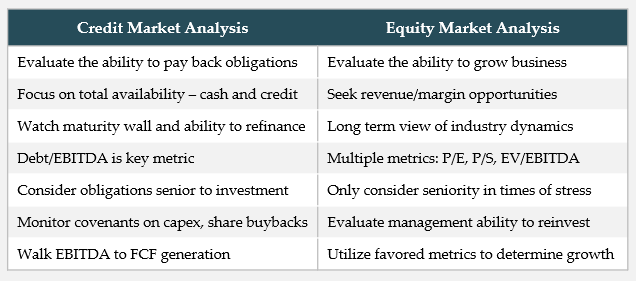

Integrated Credit and Equity Analysis

Credit Market Analysis vs Equity Market Analysis. The key difference between credit and equity investors is incentives. Credit investors have limited upside while equity investors have unlimited upside. The credit investor is therefore heavily incentivized to sniff out trouble to avoid losses, focusing on cash flow metrics over accounting profit. While an equity investor focuses on improving sales and margin potential, they often miss deteriorating bond prices, issuer ratings, or maturity walls.

Penn Capital first determines if a company is credit worthy before considering an equity investment. The credit market provides strong signals, for both individual companies and the overall market, that can improve equity returns. Credit and equity research integration can enhance the depth and breadth of traditional equity analysis.

For more information on the topic, our research can be found here.

A PDF version can be found here.

*Russell 3000 Index companies per S&P issuer ratings as of 10/31/2019, source: Bloomberg.

The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Under no circumstances should this information be construed as a recommendation or advice. The views expressed herein reflect the professional opinions of the portfolio managers and are subject to change. Penn Capital does not accept any liability for losses either direct or consequential caused by the use of, or reliance upon, this information. These views are subject to change at any time and they do not guarantee future performance of the markets. Investing in the stock market involves gains and losses and may not be suitable for all investors. Investors have the opportunity for losses as well as profits.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Penn Capital), or any non-investment related content, made reference to directly or indirectly contained within this commentary be suitable for your portfolio or individual situation, or prove successful. Comparisons to indices are inherently unreliable indicators of future performance. The strategies used to generate the performance vary from those used to generate the returns depicted in the benchmarks. Penn Capital makes no representation as to the methodology used to generate the benchmark returns. Portfolio holdings are subject change and may or may not be held by one or more Penn Capital portfolios from time to time. Transactions in such securities may be made which seemingly contradict the references to them for a variety of reasons, including but not limited to, liquidity to meet redemptions or overall portfolio rebalancing.

The Russell 3000 Index is a market-capitalization-weighted equity index maintained by the FTSE Russell that provides exposure to the entire U.S. stock market. The index tracks the performance of the 3,000 largest U.S.-traded stocks which represent about 98% of all U.S incorporated equity securities.

A copy of Penn Capital’s current written disclosure statement discussing our advisory services and fees is available upon request.